Insurtech vs. Insurance

Millennials are driving change in the insurance industry. Unlike their parents, they have not jumped into insurance with two feet. Many are even skipping vital insurance products such as life insurance. The reality is that ZMillennials (Millennials and Generation Z) don’t have faith in the insurance industry. Many see it as repetitive, untrustworthy, archaic, and an industry only after their hard-earned money. However, this does not imply that ZMillennials do not care about insurance. A product that addresses their demands simply has to be different, above all offering transparency and flexibility through digital interactions.

This is particularly important because studies suggest that ZMillennials decision making process, partly due to their large numbers will have an impact on any business industry. For example, the fact that ZMillennials prefer the sharing economy has had an impact on the car industry. Furthermore, the fact that this group is not buying houses (preferring home-sharing/renting), unlike their parents, will have a multiplier effect not only to the construction industry, but also the insurance industry as home insurance uptake will be affected.

Why disruption is now a reality in Insurance

Traditional Insurance, as we know it, is stale!

Look at the top insurance companies in the world. Most have been in business for over 100 years. However, this does not imply that they no-longer serve an important role. But, just like all established companies in other industries they cannot transform into a digital-first organization over night. Extensive physical infrastructure, limited digital capabilities and overly established go-to-market strategies guarantee a profit at the expense of offering a customer optimal experience.

Nevertheless, incumbents have realized they need to change and many of them are taking big steps to satisfy increasing demands by the digital fluent customers. Those are constantly questioning long-held beliefs about business structures and their relevance today. For example, why should one pay fixed insurance premiums instead of paying on the go, why not only when actually exposed to risks?

As the wind changes, it’s time to adjust the sails

Traditional players for a long-time treated

Big data and analytics backed by strong cloud foundations was and still is a game-changer. Insurance is now shifting from a descriptive model of what happened to a more predictive model of determining a fair outcome for everyone involved. This shift is aiding insurance companies in ensuring with a high degree of certainty of what will likely happen in addition to responding proactively. The result is that insurance firms are now in a better position in eliminating fraud cases, better listening to customers concerns and acquiring new customers.

How Insurtech is winning over

Insurtechs are making inroads primarily in the personal retail space. An estimated 75% of Insurtech serves retail clients with the rest making inroads in the commercial sector. Online and mobile channels have provided a convenient route in acquiring customers who are tech-savvy, who are demanding on-the-go products, eliminating physical interaction in receiving insurance quotes and submitting claims.

As underlined by Mckinsey, Insurtechs are successful due to the following:

- Through Social Engagements – Insurtechs are changing the whole conversations on the relationship between the insurer and the company. Many are adopting the model where insurance acts as a

value added service. The customer has an opportunity of discussing insurance aspects openly in an engaging manner. This social contract assurespolicy holders that they have a listening and open partner. - Digitizing moments of truth – this is particularly important when making claims. Traditional insurance companies are designed to make it difficult to get insurance claims. This potentially is an area of concern for many and to some a

deal breaker . By digitizing this process either by taking photos of an invoice and sending them instantly to insurance providers to initiate the claim process makes the process transparent. One such company that has successfully implemented this isBauxy . Entrepreneurial spirit of founders – Insurtechsare often ran by founders who are tech-savvy and not burdened by heavy operation expenses or cultures often found within incumbent organizations. They tend to go forflat organization style and this way they attract employees who can easily identify with the company mission and vision. This way manyinsurtechs easily make adjustments andadopt to process that work.

What does this mean for established players?

Looking at the bigger global picture, Insurtech is still a tiny fraction. For established players, this is not the time to panic, at least not yet. For starters, many insurances still rely on established players to underwrite risks. Approximately 61% of insurtechs are primarily driven by the needs of the insurance industry players. About 30% are focused on disintermediating customers and only 9% want to completely replace established players.

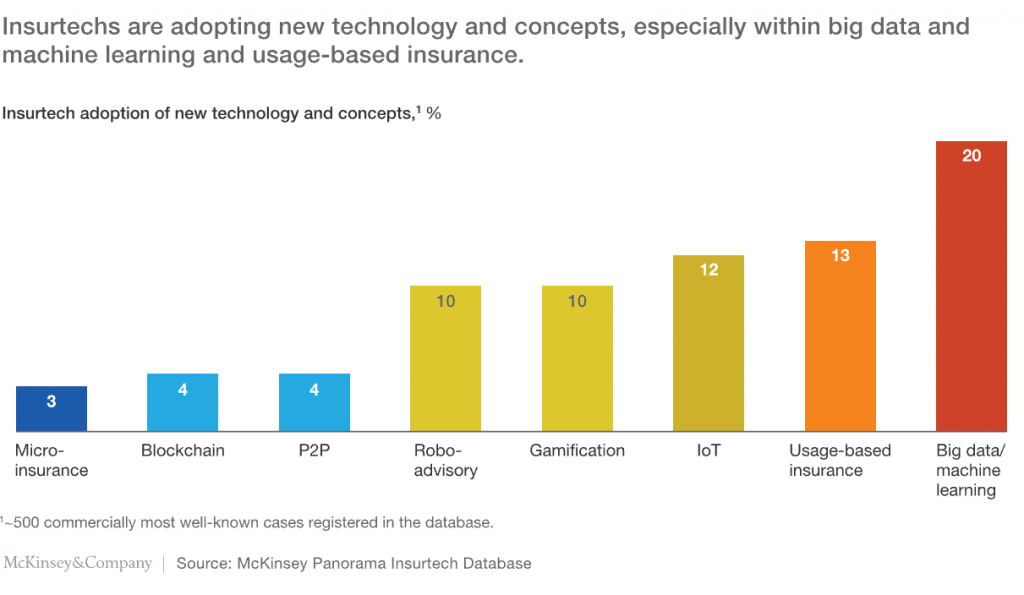

Established players have the advantage of understanding the “game”, and data collected over the years gives them the upper hand. The fact that they have deep pockets either for acquisitions or partnership is also an advantage. To be able to survive in the days ahead and especially appeal to ZMillennials, the need to adapt to what resolve their dilemma of going digital or vanish. Technologies and concepts they will need to adopt in one way or another are those listed in the graph below:

They need to assess business models and address pain points that can solve collaborating with

For the growth of Fintech and the threats or opportunities offered to banking provides a relevant example. Fintechs once overlooked by established banks are today key players in the market. When their threat became apparent, some banks opted to invest in them; others opted to incorporate their business models while others rightly bought competing Fintech. Traditional players can utilize the power of Insurtech in achieving the following goals:

- Enhancing customer experience

- Assessing new markets

- Redefining their business model by shading archaic business practices and employing what can best be delivered via technology

- Appealing to younger customers

- Testing new Business models

For

In all these realignments, the ultimate winner will be the customer. As insurance becomes demystified and more players join the party, the days of non-centric customer interaction and rigid data mining will slowly be forgotten.

*Spot on with this write-up, I truly think this website needs much more consideration. I?ll probably be again to read much more, thanks for that info.

Heya! I’m at work surfing around your blog from my new iphone! Just wanted to say I love reading your blog and look forward to all your posts! Carry on the fantastic work!

Valuable information. Lucky me I found your website by accident, and I am shocked why this accident did not happened earlier! I bookmarked it.

Hello! I could have sworn I’ve been to this blog before but after browsing through some of the post I realized it’s new to me. Anyways, I’m definitely happy I found it and I’ll be book-marking and checking back frequently!

I am so grateful for your post. Fantastic.